Cutting To The Chase

Cutting To The Chase

The Fed's Battle Is One Of Relevance

September 16th, 2024 - Volume 10 (2024), Missive 212 (Monday)

This week’s Fed cuts are too long in coming

The curves believe the change in heart is only half-hearted

Banks will fight against lower rates

Those who do, can. Those who don’t are passed over for those who are willing and able. These garbled statements are not the product of some centuries old philosophy, but rather our poor attempt to qualify what a quantifiable mess the approach to monetary policy has been these past few years and an economy that has lost almost all patience with the financial sector’s ability to come through. All of this begins and ends with surplus productivity, of course, which by itself isn’t the issue. The problem stems from this force being allowed to spread across the entire economic landscape, not only unencumbered by the Fed, but also amplified by it through the mistaking of price volatility for price inflation. Now as the upward price volatility subsides in the product market, the downward price volatility in the resource market, specifically that of the labor market, is on much fuller display; something not easily remedied by an institution that works through a displaced financial sector in order to achieve economic goals.

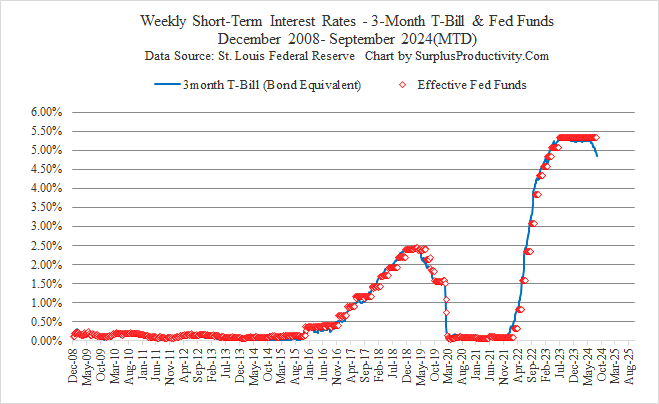

The short-term Treasury market knows the Fed has pushed rates way too high for way too long.

It always comes to a bit of shock to many when they realize the Federal Reserve is an institution set-up to use the economy’s financial sector in order to achieve economic goals and not the other way around. Just like the fallacy of printing money (controlling the supply of money has nothing to do with the actual quantity of currency and everything to do with the quality of currency, more on that for a future missive), the Fed isn’t charged with being a ‘lender of last resort’. What they are in charge of is ensuring

Keep reading with a 7-day free trial

Subscribe to SurplusProductivity.Com to keep reading this post and get 7 days of free access to the full post archives.