A Most Dangerous Path For Policy

Frightening Journey Can Only Lead To Nightmare Results

July 10th, 2025 - Volume 11 (2025) Missive 105 (Thursday)

There’s no middle in the Fed’s job

10yr Treasury auction results point to liquidity grab

Inflation expectations more than anchored

“Participants noted that the Committee might face difficult tradeoffs if elevated inflation proved to be more persistent while the outlook for employment weakened. If that were to occur, participants agreed that they would consider how far the economy is from each goal and the potentially different time horizons over which those respective gaps would be anticipated to close.” - June 17th-18th FOMC meeting minutes released July 9th, 2025 (emphasis added)

Its a dangerous thought, but still fortunately just a thought. At the same time, it is becoming pervasive which is all the more troubling. Of course, the thought we are alluding to, and pulled out in the above quote from the FOMC’s latest meeting minutes, is the notion that, somehow, policymakers can achieve one of their Congressionally goals without the other. That, however, is an economic impossibility due to the fact that both goals are either achieved or missed concurrently due to the shape of the output gap at any given point in time. As such, it is concerning to say the least, that policymakers are continuing to ponder a situation where a time exists that one goal is met and the other isn’t.

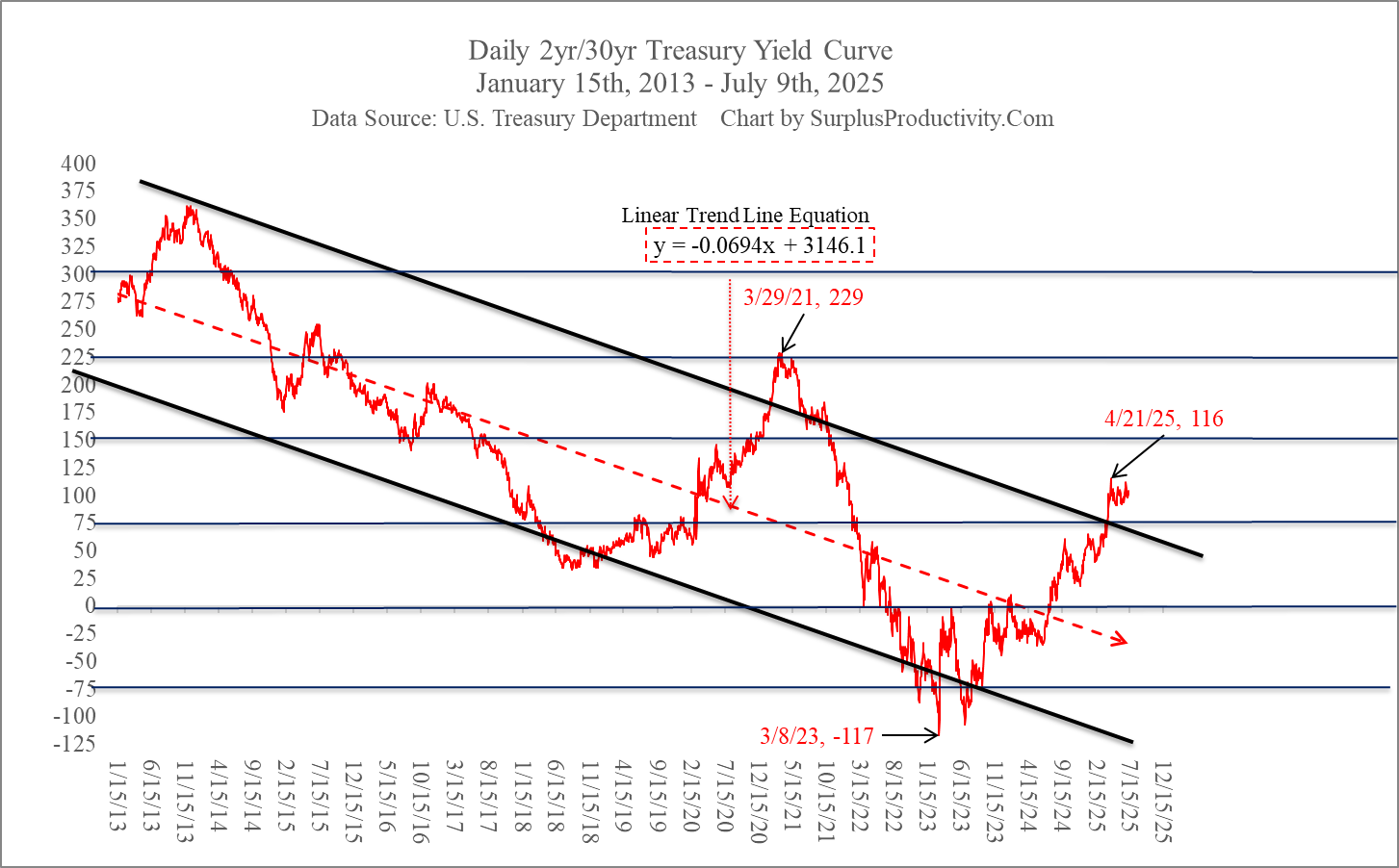

The Fed can either attain stable prices and full employment at the same time or they can’t achieve either as both are simultaneously controlled by the state of the output gap which is measured mostly by the shape of the U.S. Treasury yield curves.

Time is and isn’t on the Fed’s side when it comes to managing monetary policy as they have adequate resolve in the longer-term to set thing right but significant consequences in the nearer term the further they are from the correct course. It is shocking, therefore, to see at least some of the participants at the Fed, assuming the luxury of a time where one goal can be met and another not. More specifically, its

Keep reading with a 7-day free trial

Subscribe to SurplusProductivity.Com to keep reading this post and get 7 days of free access to the full post archives.