For Capacity's Sake

Plenty of room in the economy

May 15th, 2026 - Volume 12 (2026) Missive 62 (Friday)

Labor’s power play is over

Capacity utilization rates too low for inflation

Treasury yield curve’s down to its old tricks

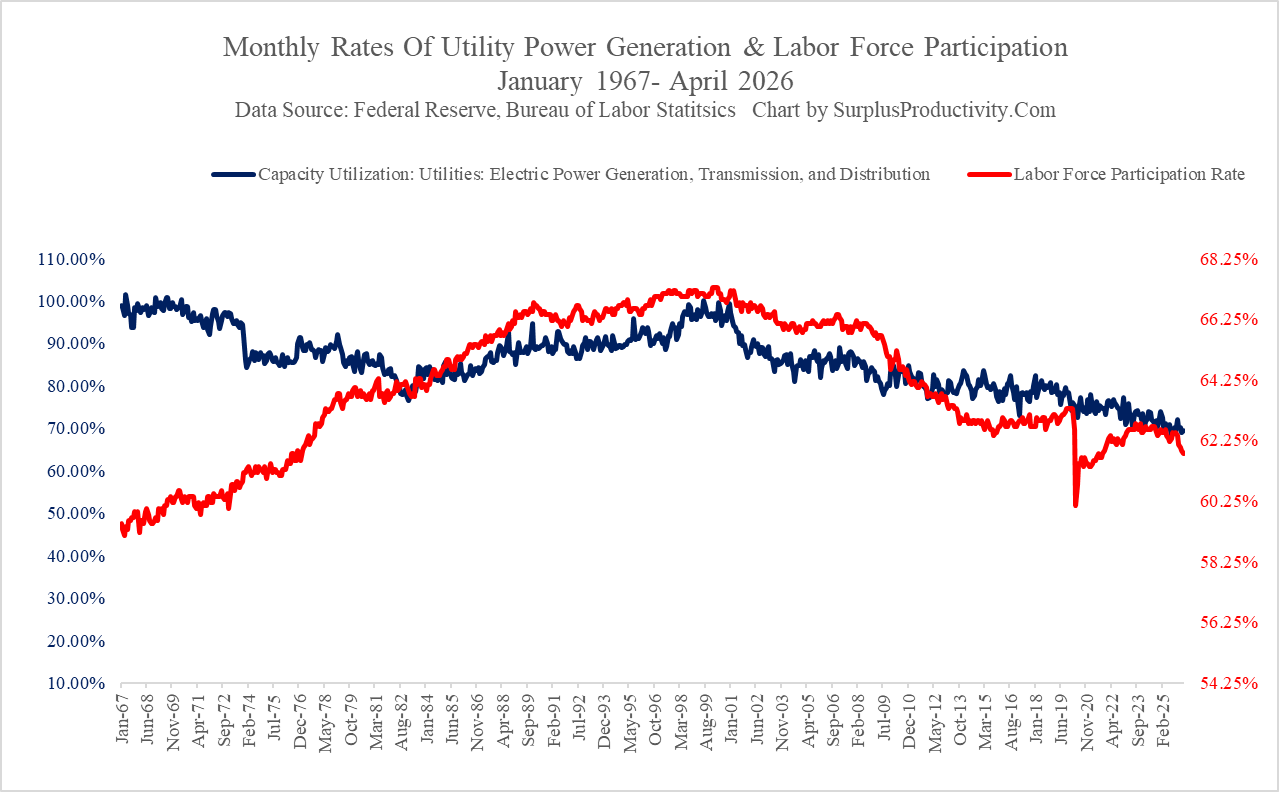

The Federal Reserve made public its latest industrial production report which not only tracks goods output for the month but also, and what we believe is more important, the sector’s current usage of physical capacity. The closest economists have to an economic indicator to the economy’s output gap, the capacity utilization data gives a sense as to just how ‘hot’ or ‘not’ the goods sector is running up to its physical limits of production. We can then, in turn, paint that dynamic with a fair degree margin of error included over the entire economy. This analysis has never been flawless and, given the general shrinking of the goods sector in terms of overall share of the economy’s output, has been less potent over the years. Yet, a very strong correlation still exists between overall rates of capacity utilization and monetary policy. Another is the relationship between the rate of utility power generation capacity utilization to that of the labor market; something that may actually be breaking down in-front of our very eyes.

Labor’s power play may be coming to an abrupt end.

The relationship between the labor force participation rate to that of electric power utilization has been a positive one for much of the last 50 years for obvious reasons. With more work to be done, and more workers around to do it, the rate of utility power capacity utilization rose dramatically throughout much of the 1980s and 1990s. This corresponds strongly to that of the labor force participation rate which was also expanding quite briskly over that same time frame. However, as labor force